The monthly deficit of the current account of the balance of payments that emerged in July for the first time in four years is the result of a combination of one-off factors and seasonality, experts believe. The current account in the first half of the year (especially in the second quarter) remained in noticeable surplus and was only slightly below the long-term average. This serves as a foundation for supporting the ruble exchange rate — against the backdrop of the Central Bank's also strengthening it interventions under the budget rule. The situation with imports adds uncertainty to the exchange rate picture, although analysts' assessments of the current dynamics and prospects for imports differ.

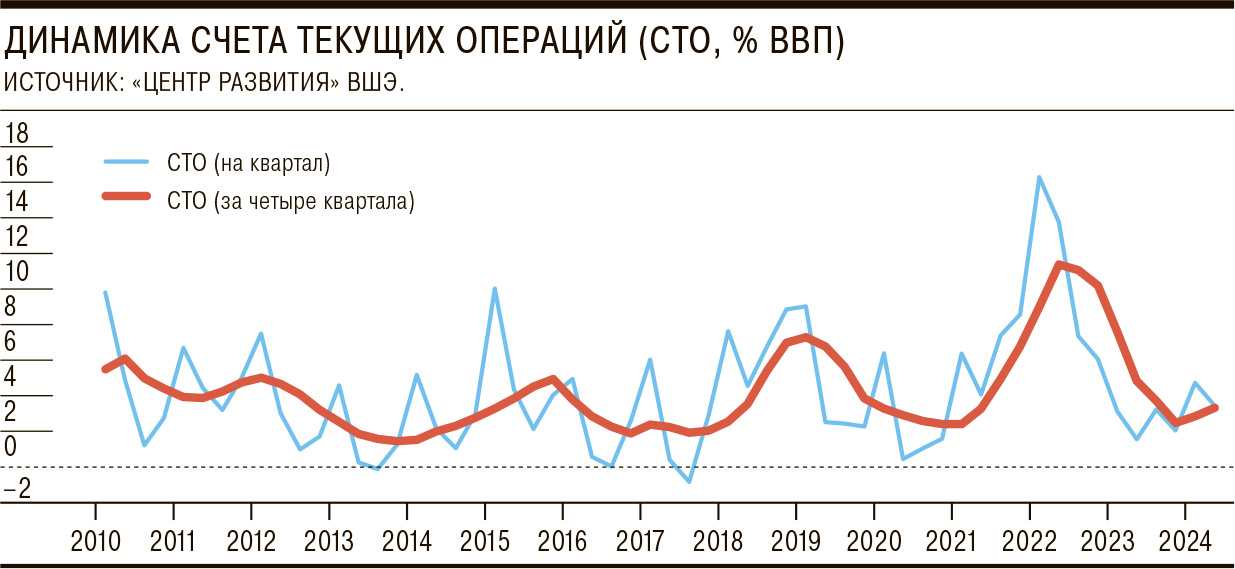

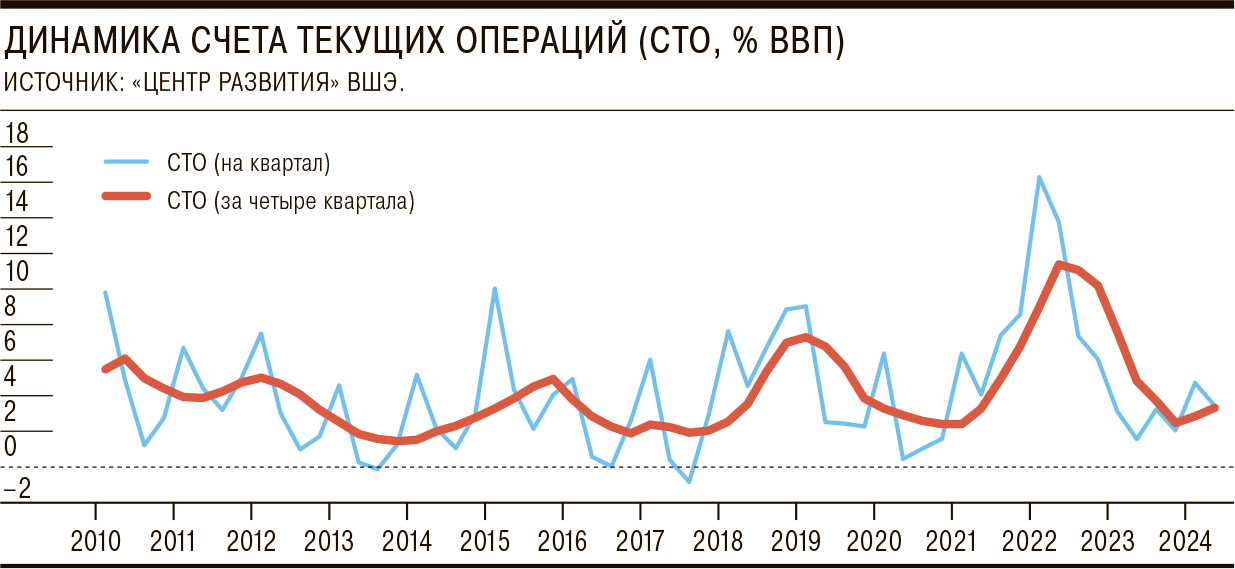

Discussing the Central Bank's estimate of the current account deficit of $0.5 billion (the first since August 2020) published on Tuesday, analysts agreed that it was a «random outlier.» On average, taking into account the last four quarters (shifted year), in April-June the current account surplus was 3.3% of GDP (3.5% of GDP in July), which is not much less than the average of 4.5% of GDP since 2010, according to economists from the HSE Development Center (see chart).

«The deficit in July is largely «paper» due to the inclusion of non-resident dividends, which are credited to type «C» accounts,» explains Dmitry Polevoy from Astra UA. This is indicated by the growth of external liabilities by $3 billion, he adds, noting that foreign assets grew by $4.7 billion, which ensured a net capital outflow of $1.7 billion — the minimum since July 2023. «Due to restrictions on capital movement, this is neutral in terms of impact on the ruble,» Raiffeisenbank analysts add.

Analysts explain the July decline in the surplus of foreign trade in goods and services (to $3.9 billion — the minimum since January 2024) by seasonality.

However, their estimates diverge here due to different approaches to eliminating it. «Trade balance components remained stable month on month, including imports, the decline of which was expected amid difficulties with making payments,» Raiffeisenbank economists believe based on July data. Stabilization of the cost of exports and imports of goods (seasonally adjusted, month on month) was recorded at the end of the first half of the year by analysts at the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF). Exports of goods were about $35 billion per month from August 2023 to June 2024, and imports for the same period were $24 billion per month. «The slight revival of exports that was emerging did not consolidate (which is natural in the context of tightening sanctions and increasing self-restrictions within OPEC+). We can talk about stabilization at a low level, after a long decline, starting from mid-2022. There is a possibility of a new decline given the restrictions on the export of petroleum products and the fulfillment of OPEC+ quotas. The growth of consumer (and, with certain reservations, investment) imports will likely lead to a resumption of import expansion,” the center’s analysts believe.

“The dynamics of imports in the coming months may still worsen against the backdrop of sanctions pressure, which, all other things being equal, is just as positive (as a decline in exports.— “Kommersant”) for the ruble,» Raiffeisenbank disagrees. Analysts at Astra UA and the HSE Development Center also back this. The latter's estimates for the first half of 2024 even reveal that, taking into account seasonality, quarter-on-quarter imports contracted for the fifth quarter in a row in April-June, despite high domestic demand. This, in their opinion, was the main reason for the ruble's strengthening in the last three quarters. Dmitry Polevoy, in turn, notes: in rubles, the seasonally adjusted value of imports of goods and services in July decreased by 11.8% against a growth of 3.1% in June, due to its reduction in dollars and a slight strengthening of the ruble, and by February 2022, July imports amounted to 85.3% against 90.9% in June and 90.6% on average for the first half of 2024, which is the maximum decrease since February 2023.

Despite the difference in estimates of changes in imports, most observers bet that at least until the end of the year, despite exchange rate fluctuations (heterogeneous exchange rate dynamics in different segments, the local dollar/yuan cross rate has deviated significantly from the global one), the ruble is not seriously threatened.

“The pace and timing of the normalization of the situation is still difficult to assess due to its unprecedented nature (but, based on historical experience, adaptation should happen fairly quickly),” they say at Raiffeisenbank. “Oil continues to trade at good levels, gas prices are rising, and fears of a global recession are receding,” concludes Dmitry Polevoy, noting that the problems of revenues from declining exports are offset by the Central Bank’s interventions within the framework of the budget rule. We note that analysts are not yet seriously discussing the scenario of increasing imports and decreasing exports.

Свежие комментарии