When a difficult decision is looming, it helps if someone else can make it first and take the blame if things go wrong not this way.

This is the situation facing much of the global central banking community.

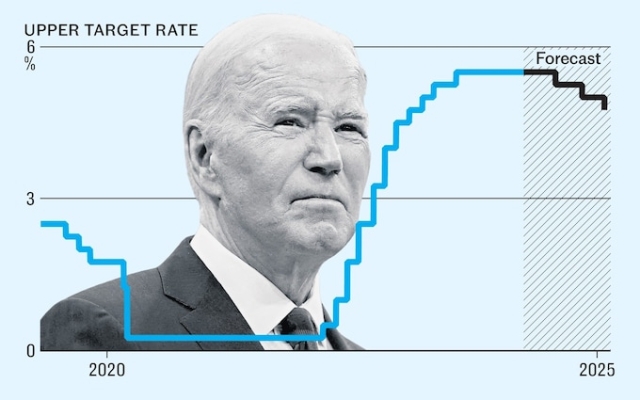

Almost all have raised interest rates to fight inflation and are now looking to cut borrowing costs again. down again.

The difficulty is when it works.

Luckily, June provides a great opportunity. The first meeting of the European Central Bank will take place on June 6, followed by the US Federal Reserve a week later and the Bank of England shortly after.

This means Andrew Bailey and his Threadneedle Street colleagues can wait until the Fed meeting. – and it is advisable for the ECB too – to act and then follow suit.

But even as the eurozone's weak economy appears to be calling for a rate cut, American power, pumped up by Joe Biden's heavy borrowing and spending, is roaring and could thus require rates to stay high even longer. Traders in financial markets are now postponing their forecasts for the first US rate cut to July.

Recent US inflation data shows that price growth remains stubbornly high. Headline inflation, as measured by the consumer price index (CPI), was 3.2% in February, while core inflation, which does not take into account volatile movements in food and energy prices, showed prices were 3.8% higher than a year ago back.

The Fed's preferred measure of inflation, based on the Personal Consumption Expenditures (PCE) index, is currently 2.5% — or 2.8% excluding food and energy. All indicators remain above the central bank's target of 2%.

Goldman Sachs analysis found housing costs remain a key factor. With costs up 6% from last year, that's double the average over the past two decades and well above the Fed's 2% target.

Restaurants and other leisure spending also remain key drivers of inflation, while spending on hotels and furniture is much lower.

Goldman also highlighted that while energy prices are currently at 138% of pre-pandemic levels and wage growth remains strong, there are signs that the labor market is cooling. Goldman believes inflation will return to the Fed's 2% target by next year.

But Pimco, one of the world's largest bond investors, said growth in the world's largest economy remained «surprisingly strong» and was likely will continue compared to other G7 countries.

“We continue to expect the Fed to begin normalizing policy mid-year, similar to other developed market central banks. However, subsequent Fed rate cuts could be more gradual,” said Tiffany Wilding and Andrew Balls of Pimco.

“Factors that have contributed to US resilience may continue to support the (still slowing) economy. for some time yet,” they added, citing five reasons why the US economy is likely to remain strong.

One of the main factors, they said, was Biden's increased spending during the pandemic. “The continued high federal budget deficit has strengthened demand in the U.S. relative to other regions.”

The US deficit in 2023 was $1.7 trillion (£1.35 trillion), or 6.3% of GDP.

Pimco also called the upcoming US election a “watershed moment,” which nevertheless suggests both candidates are “leaning toward policies” that will stimulate economic growth and borrowing.

The Fed's decisions have implications for the rest of the world, in part because its analysis is taken into account by other central bankers studying the likely path of inflation. In addition, because the Fed is the most powerful monetary authority in the world, its interest rates affect borrowing costs around the world.

Traditionally, the Fed has been considered the leader in monetary policy, with the assumption that when it changes interest rates, others will follow.

As a result, one might assume that a later move by Fed Chairman Jerome Powellmeans that Bailey and the ECB, led by Christine Lagarde, may also remain on the sidelines.

But that is not the case Always. The Bank of England was the first to raise interest rates in December 2021, before the Fed joined in the action in March 2022, well ahead of the ECB, which held off until July that year.

“Recent history shows that this is not the case. necessarily true — we deviated, we were the first to raise the rates, so why not lower them first? says Martin Beck, chief economic adviser at the EY Item Club.

“The US economy is really strong in many respects and we are not, so there is not as much pressure to rein in activity as there is now.”

However, there are three other key reasons why Threadneedle Street might want to take notice. on the actions of his American counterpart: Powell's analysis of the inflationary pressures facing the economy; potential impact on exchange rates; and the impact on global borrowing costs.

Inflation in the United States is supported in part by a tight labor market. The hot economy created a huge demand for workers, which drove up wages and thus stimulated inflation.

Wages have also become a headache for the Bank of England, with UK wages still rising at more than 6% a year.

“The question will be whether there are any similarities between the US and UK, which suggest some risks with rate cuts,” says Rob Wood of Pantheon Macroeconomics.

“In the case of the UK, the labor market remains tight, wage growth is higher than in the US, inflation remains higher, at least until the next issue, and economic growth, according to business surveys, is accelerating quite sharply.”

The situation in the eurozone is somewhat different. Although its labor market has recovered from the pandemic, unemployment at 6.5% is still much higher than Britain's 3.9%, giving Lagarde and her colleagues less worry about a wage-price spiral.

Then comes the exchange rate. rate threat.

The UK has almost overcome the wave of imported inflation driven by energy prices and international food markets.

If it moves ahead of the Fed, it risks causing a depression in the pound and thus raising the cost of imports again.

p> “If you move significantly further and faster than the Fed, you may find yourself generating more inflation as the pound falls, which would be quite uncomfortable if you've just been through a period of dealing with very high inflation,” says Pantheon's Wood.

Regardless of the exact timing of the Bank of England's first rate cut, higher US borrowing costs will have an impact on this side of the Atlantic, so even if the UK does lead the attack, the effect risks being decidedly underwhelming.

p>“This makes monetary conditions around the world tighter than they otherwise would be because the US is the dominant player,” says Beck of the EY Item Club.

“Market rates in the UK are will still fall due to the Bank of England's spending cuts, but the fall will not be as strong due to the gravitational pull of investment in the US, where yields are higher.

Свежие комментарии