A sharp increase in the key rate by the Bank of Russia in the long term will not stop the growth of the dollar against the ruble, experts believe, but they still do not advise buying the currency. In their opinion, it is better to increase the share of ruble bonds in the portfolio.

Uphill bets

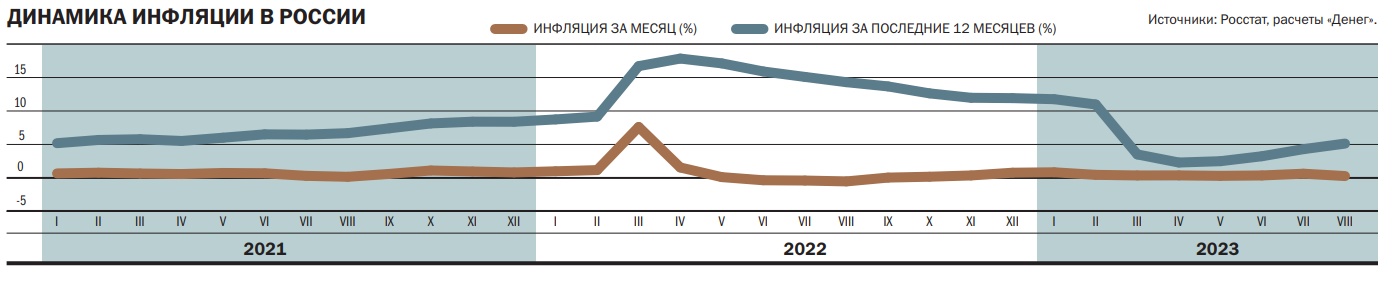

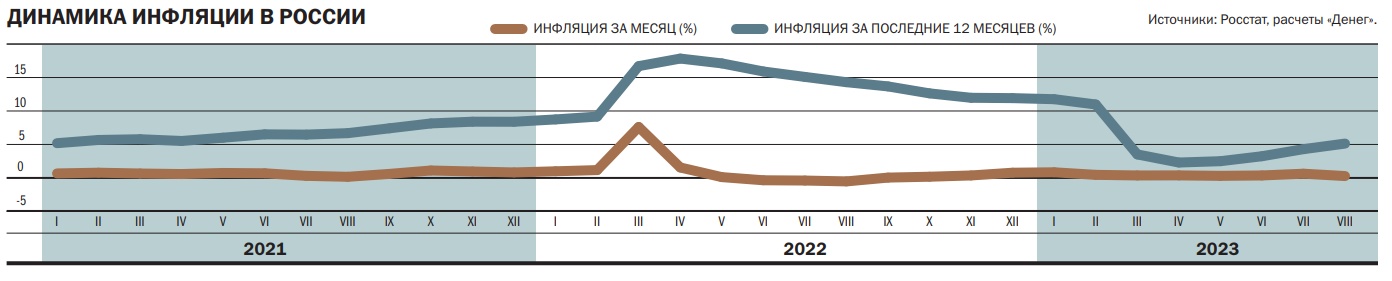

In July, the Bank of Russia moved to sharply tighten its monetary policy (MCP), starting a cycle of increasing interest rates. First, on July 21, the Central Bank’s key rate was raised by 100 basis points (bps) — from 7.5% to 8.5% per annum. The regulator explained his decision then primarily by the desire to fight inflation — the rate of price growth has accelerated and continues to grow, and inflation expectations are also growing.

According to economists, against the background of rising wages and other payments, consumer demand is also growing, but the economy, due to the lack of sufficient resources, does not have time to satisfy it. Inflation expectations are fueled by a significant increase in the dollar/ruble exchange rate, and the ruble exchange rate, in turn, is declining due to a deterioration in the trade balance: demand for imports is growing against the backdrop of a general increase in consumer demand, while exports are stagnating at best due to price pressures caused by sanctions and quantitative restrictions on the supply of products from Russian exporters.

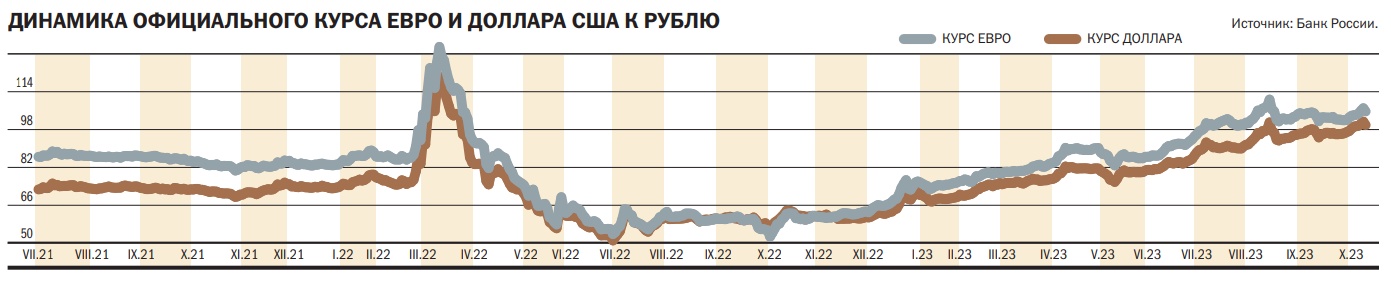

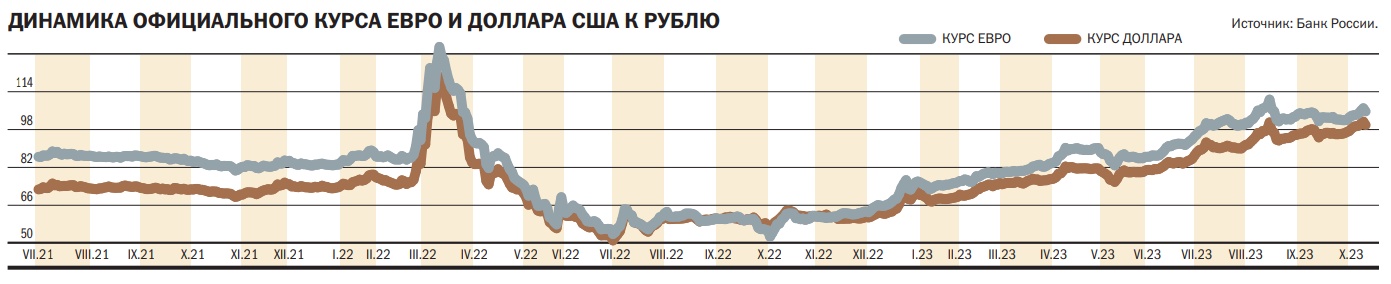

Even then, analysts noted that the Central Bank’s decision to immediately raise the rate by one percentage point was quite abrupt and unexpected for the market. But the matter did not stop there. In the following days, the dollar continued to strengthen against the ruble, and on August 15, the official rate surpassed the psychologically important mark of 100 rubles/$. On the same day, the Board of Directors of the Bank of Russia met for an extraordinary meeting and made a radical decision to immediately increase the key rate by 350 basis points, to 12% per annum. And a month later, on September 15, the Bank of Russia raised the key rate to 13% per annum.

As Olga Belenkaya, head of the macroeconomic analysis department at Finam, notes, at the same time, the Central Bank revised its macroeconomic forecast ahead of schedule. New introductions: a significant increase in budget expenditures in the bill that the government submitted to the State Duma, and higher rates of indexation of regulated tariffs in 2024, which increases pro-inflationary risks. On October 10, after a meeting of the State Duma Committee on the Financial Market, Deputy Chairman of the Bank of Russia Alexei Zabotkin told reporters that annual inflation could reach its peak value in the spring-summer of 2024. According to him, as of October 2, inflation was 5.9% year-on-year, and to return to 4%, the Central Bank plans to tighten monetary policy in 2024.

The updated medium-term forecast does not imply the possibility of reducing the key rate before the end of the year (from September 18 to the end of the year, the average key rate is projected to be 13–13.6%). “According to our assessment, the lower limit corresponds to keeping the rate unchanged until the end of the year, the upper limit corresponds to increasing the rate to 14% and maintaining it at this level until the end of the year,” says Olga Belenkaya.

“Our basic forecast assumes an increase in the Central Bank rate to 14% per annum and maintaining the indicator at this level until the end of this year. Probably, the transition to a reduction will occur in the spring of 2024, and a return to 9% in early 2025,” Evgeny Loktyukhov, head of the economic and industry analysis department of PSB, told Dengam in September. The active phase of economic recovery growth is close to completion, and GDP will most likely move to moderate growth rates due to tightening monetary policy, a noticeable weakening of the ruble and the likely prospect of the authorities switching to restrained economic stimulation, the expert believes.

“With a high degree of probability, we are already at the peak of the rate, and there are no prerequisites for its further increase,” says Evgeniy Zhornist, portfolio manager of Alfa Capital Management Company.

He believes that the main trigger for the rate increase was the sustained weakening of the ruble, which could lead to financial instability and accelerated inflation. However, to stop the devaluation, in his opinion, more effective than increasing ruble rates would be restrictive measures on the currency and measures to sell foreign currency earnings, signals about the possibility of introducing which are already coming from the financial authorities. “Having taken a pause — and perhaps a long one — the Central Bank, with an eye on inflation data, will begin to slowly and for a long time reduce the rate,” predicts Mr. Zhornist.

Artem Tuzov, Director of the Corporate Finance Department of IVA Partners Investment Company, believes that there are two scenarios for the development of events: at an exchange rate below 100 rubles. per dollar, the Central Bank will begin a gradual reduction in the rate to 7%, at an exchange rate above 100 rubles. per dollar, the key rate is likely to increase to 15%.

The dynamics of the Central Bank interest rate until the end of the year will probably largely depend on the ruble exchange rate and the level of inflation, agrees Elena Kozhukhova, an analyst at VELES Capital. However, she notes that in the current conditions of the closed Russian economy, increasing interest rates is not so effective in containing the fall of the ruble, and therefore the potential for raising rates by the end of this year may be limited to 15%. The most effective measures to support the Russian currency could be capital controls and mandatory standards for the sale of foreign currency earnings. “In case of emergency situations, the rate may be higher than 15%, but it is unlikely for a period exceeding several months,” she believes.

“If we observe a continuation of the inflationary spiral, then, in our opinion, the Bank of Russia will continue to raise the key rate,” reflects Digital Broker analyst Daniil Bolotskikh. At the end of the year, he expects inflation in the range of 6–8%.

Toxic favorite

Theoretically, an increase in rates in the national currency should contribute to its strengthening, especially since the ruble weakened significantly in the first half of the year (the US dollar exchange rate against the ruble increased by 25.7%, the euro exchange rate by 27.9%). However, in the current situation, the main driver of the ruble’s fall is not the movement of capital, but the reduction in Russia’s trade surplus, so the ruble may not strengthen.

“Now it is quite difficult to make a long-term forecast for the ruble exchange rate,” complains Daniil Bolotskikh. According to him, under the conditions of economic sanctions, changes in the key rate have little impact on the ruble exchange rate, so further movement will determine the trade balance. In his opinion, if imports were stabilized, then exports began to decline compared to March-April. Russia has extended an additional voluntary reduction in oil production and exports until the end of the year in the amount of 300 thousand barrels per day.

“Fundamentally, the ruble remains under pressure due to a reduction in the current account surplus (CTO) in the balance of payments,” says Yuri Kravchenko, head of the banking and money market analysis department at Veles Capital Investment Company. After record levels in 2022, the balance has declined noticeably this year amid a decline in exports and a recovery in imports. However, after a sharp increase in the key rate of the Central Bank and tightening of monetary conditions in the market, we can expect a slowdown in lending growth, which will limit the demand for imports and thereby slightly improve the value of the total cost. In this regard, by the end of the year you can count on the strengthening of the ruble compared to the levels of summer-autumn lows.

Finam analyst Alexander Potavin has a similar long-term forecast. “At the moment, the fundamental factors that led to the weakening of the ruble remain,” he notes. The authorities, according to Mr. Potavin, will try to stabilize the ruble exchange rate specifically before the 2024 presidential elections. After elections, according to his observations, the ruble exchange rate usually weakens. “It’s difficult to say in terms of timing, but there is no doubt that the dollar exchange rate will return to the highs that were shown in the spring of 2022, that is, to 120 rubles,” believes Alexander Potavin. By the end of this year, he expects the dollar exchange rate to be in the range of 92–102 rubles. The key reason for the weakening of the ruble exchange rate in the first half of this year, in his opinion, was the reduction in the influx of hard currency into the country, the decline in Russia's trade surplus while maintaining high demand for currency from the population, importers and businesses leaving Russia.

“We expect that the authorities will take measures to mitigate the negative impact of the declining foreign trade surplus and imbalances in its currency structure on the position of the ruble. Therefore, we maintain our forecast for the dollar exchange rate at the end of this year at around 95.5 rubles,” says Evgeny Loktyukhov.

“There is a lot of uncertainty and unknowns in the current exchange rate — what will happen to exports and imports, the budget deficit, capital outflow. But it seems that the bar is 100 rubles. reflects rather negative assessments and emotions based on retrospective analysis, without taking into account prospects. Weighing the available inputs and the risk premium in the course, the ruble can easily return to the level of 90 rubles/$,” says Mikhail Zeltser, stock market expert at BCS World of Investments.

No hope for cache

Despite the possible weakening of the ruble in the long term, experts do not yet advise private investors to shift to foreign currency assets.

“The currency of unfriendly countries is definitely not a way to preserve capital or investment,” Artem Tuzov is sure. Russia remains an export-oriented economy, and the ruble will weaken against foreign currencies, he emphasizes. Owners of non-cash dollars or euros, in his opinion, may not receive anything from this weakening if correspondent accounts in the currencies of unfriendly countries are closed to the entire Russian banking system. “Therefore, if you bet on the weakening of the ruble, it is better to do it in the currencies of friendly countries or in instruments that are traded on international exchanges for dollars, such as gold,” he concludes.

Purchasing assets in foreign currency is more of a means to diversify a portfolio than a way to earn additional profit due to fluctuations in the ruble exchange rate, says Vladimir Bragin, director for analysis of financial markets and macroeconomics at Alfa Capital. As past years show, he reminds, the Russian currency can not only sag sharply, but also strengthen, so a strategy built on expectations of further weakening of the ruble may not work. At the same time, he does not rule out that by the end of the year the ruble may strengthen somewhat, and the dollar exchange rate, accordingly, will drop to 80–85 rubles. “Investors in the current environment do not have many options for investing in currencies: in addition to replacement bonds denominated in dollars and euros, you can buy instruments in yuan or invest in Hong Kong dollars, but the Chinese currency can also be very volatile and will not protect capital in the event of a strong dollar strengthening,” adds the expert.

From equity to debt

As for ruble financial instruments, according to Yuri Kravchenko, in connection with the increase in the key rate of the Central Bank, an increase in bond yields and rates on bank deposits is already observed. In his opinion, by the end of this year, deposit rates and bond yields may reach local maximums.

“Short-term deposits should reflect the soaring rates. The same is with loans, so if the planning period is sufficient, then it is better to wait with a temporarily expensive loan, and place existing savings in OFZs with the prospect of normalization of yields and rising bond prices already in 2024, since autumn purchases of securities in 2023 in a year may bring significant capital gains,” reflects Mikhail Zeltser.

Now money market funds look very attractive: there you can get a return close to the key rate, which is now at the level of profitable corporate bonds, believes Evgeniy Zhornist. In the medium and long term, in his opinion, corporate bonds also look attractive.

“The increase in bond yields against the backdrop of a rise in the key rate allows us to gradually rebalance the portfolio from stocks to short-term bonds with a yield that is satisfactory until maturity,” says Artem Tuzov. “Previous periods of growth in the key rate at the beginning of 2014 and in mid-2021 occurred before a serious correction in the stock market; a significant part of the portfolio in short bonds allowed investors to go through these periods with minimal losses,” he recalls. At the same time, according to his observations, the stock market has grown quite strongly this year and a correction can be expected there during this period of growth of the key rate.

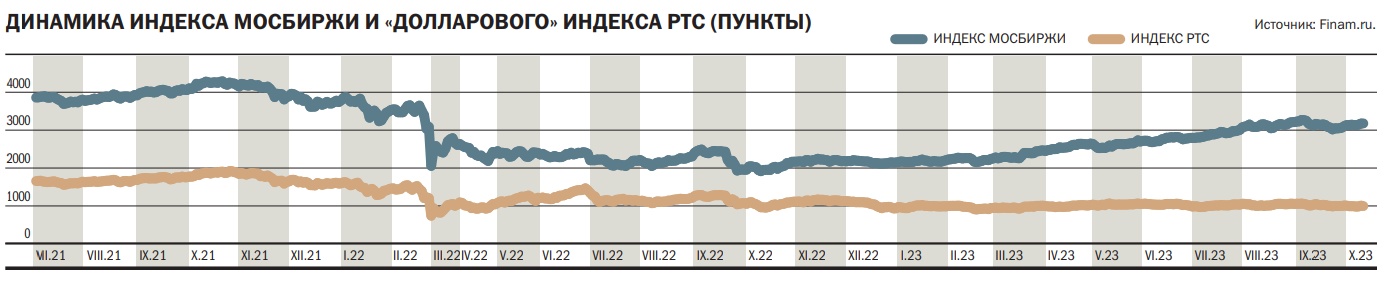

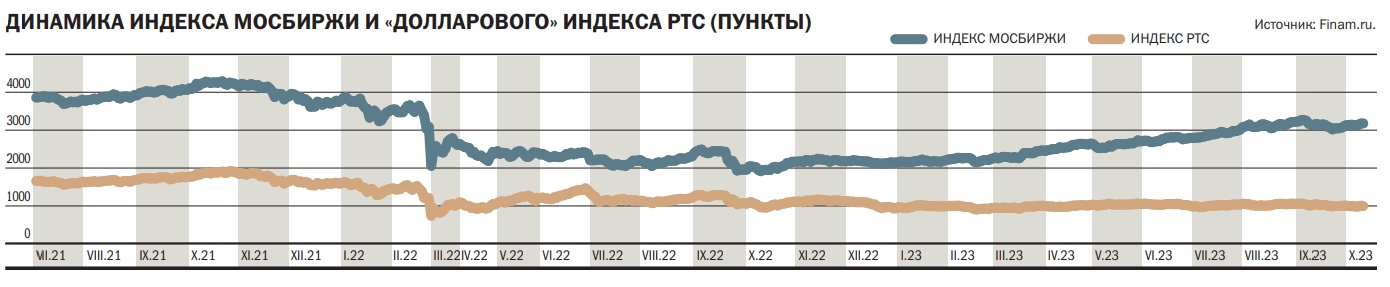

Daniil Bolotskikh also expects a correction in the stock market. “Globally, we believe that the Russian stock market is valued quite low,” he says. However, he notes that the growth of the Moscow Exchange index has continued since March and, against the backdrop of an increase in the key rate and the growing attractiveness of debt instruments, it would be nice for the stock market to go into a correction in order to continue its steady growth until the end of the year. The expert believes that after a sharp increase in the key rate, dividend stories lost their attractiveness, so for the rest of the year, he names bank papers, growth stories and “relocation” (redomiciliation) of domestic companies registered abroad to Russia as favorites on the stock market.

Mikhail Zeltser is more optimistic about equity securities. For the stock market, a high rate, according to him, is negative, but there are other factors in the price dynamics of securities — dividends, the accelerated process of redomiciliation, he explains. “Now the market has grown by almost 50% since the beginning of the year, and a technical correction in the Moscow Exchange index and securities is not excluded, but this could be an interesting opportunity to enter the market with the idea of further growth. In 2024, our estimates boil down to a rise in the Moscow Exchange index to 4300 points, that is, an increase of about 40% from the current value, and if a temporary decline in securities prices does occur in October, then the final return for the period may be even higher,” — the analyst believes.

“An increase in the key rate may limit the demand for securities of companies that consistently pay moderate dividends, for example, MTS and representatives of the electric power industry,” says Evgeny Loktyukhov. It is worth looking more conservatively at companies with large debt loads. Among the domestic sectors, in his opinion, shares of banks and the consumer sector look the most advantageous. “In the medium term, in our opinion, it is worth increasing the share of exporters in portfolios. First of all, you can pay attention to shares of oil companies and representatives of the transport sector. We also believe that the bond portfolio should be diversified in favor of securities with floating coupons, linked to RUONIA or the key rate,” adds the analyst.

Свежие комментарии