In less than a week, Andrew Bailey began his new job as Governor of the Bank of England as politicians crossed the Rubicon.

< p>It was March 2020 and the Bank had just started printing money to the tune of £200 billion to calm financial markets as it became clear that a lockdown was looming. The money will be spent on government bonds held by banks to free up cash in the system and keep the economy moving.That same day, however, marked the first burst of so-called quantitative easing (QE) during the pandemic. Before then, Chancellor Rishi Sunak announced a furlough scheme that would subsidize wages by up to £2,500 a month.

Reflecting on the events of that weekend, Bailey admitted to colleagues that the Bank was «de facto financing the government deficit» by collecting debts already held by commercial banks, freeing them up to buy newly issued bonds.

«Our predecessors will be turned around in coffins,” sources recall him saying in his note, although Bailey was also quick to point out that the Old Lady is not the only central bank that effectively prints money to finance the government.

At the Treasury, Sunak was in a state of panic after a usually walking auction of short-term Treasury bills failed to attract enough demand, something that had not happened since 2008.

The former chancellor estimated he would need up to pounds sterling. $500 billion worth of debt will be issued to ensure the government can pay all its bills.

Bailey told Sunak on the phone that he believed monetary financing — printing money to directly fund the government — was unacceptable, although the governor later publicly admitted it would be difficult for the government to finance itself if the Bank had not intervened.

Recognizing that the Bank was in uncharted waters in unusual times, Bailey even floated the idea of creating a mechanism that could buy British shares, something consultants say was done in the 1930s, to support the economy.

In the end, the Bank stuck to bonds, accumulating more than £850 billion at its peak.

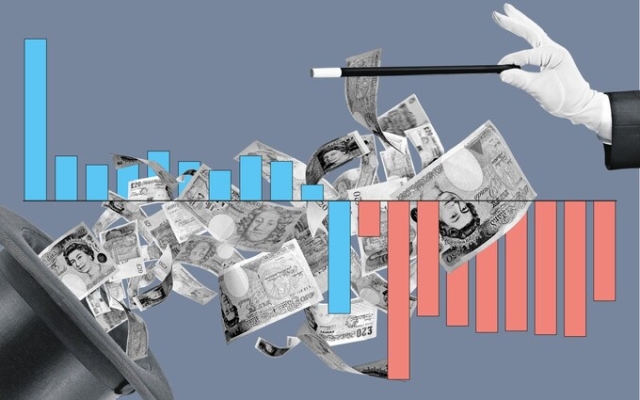

Many economists and politicians believe QE helped fuel inflation. However, this is not the only cost of this policy. The costs of maintaining this huge stock of debt rise as borrowing costs rise.

In the second of our three-part debt series, we examine the true cost of the Bank's money-printing program and reveal how poor policy choices could end up costing taxpayers tens of billions of dollars in the coming years.

Everyone has argued from the beginning that know QE is not free money.

The new policy was always intended to be temporary and unusual, born out of necessity in the midst of the global financial crisis.

When Labor Chancellor Alistair Darling first allowed the so-called Asset Purchase Facility (APF) to raise £50 billion of bonds in January 2009, he assured the public that the impact on public finances would be «largely temporary» and the assets would be «held» . no longer than necessary to ensure stability and protect the interests of taxpayers.”

Lord King, then governor of the Bank of England, also stressed in a letter to Darling that Threadneedle Street would wind down its portfolio of assets when the situation returns to normal and «consider appropriate arrangements» for their sale, «taking into account the impact of these sales at the prices achieved.» In other words, the Bank will be careful not to flood the market with securities and distort prices.

Officials put financial stability and value for money at the heart of any intervention. However, it quickly became clear that purchasing bonds was becoming a serious tool for making money for the Bank.

QE works by creating reserves that commercial banks hold as deposits with the Bank. Threadneedle Street pays interest on these reserves at the current base rate.

When interest rates were at a record low of 0.5% and then 0.1% during the pandemic, the Bank earned much more on income from government bonds than before. bought it and had to pay interest. The Old Lady was profitable.

As revenues grew, the government began to take notice.

Andy King, who at the time worked at the Treasury as a civil servant and then as an official at the Office for Budget Responsibility (OBR), the government's tax and spending watchdog, says: «It grew and when we reached 20 billions of pounds sterling, ideas suddenly started coming in about what could be done with them. That's when the Treasury decided that having a big, tempting pile of money reported every quarter wouldn't work because it was simply impolitic. I can handle it.”

In 2012, Chancellor George Osborne made a decision that still has consequences today: he decided to start transferring those profits to the Treasury.

Osborne said the move would allow government to “manage its cash more efficiently.” insisting that the move was «solely for the benefit of public finances and debt reduction.»

Everyone else saw through the accounting trick that allowed him to carry out a multibillion-dollar raid on QE profits.

Lord Macpherson, then permanent Chancellor of the Exchequer, says: “They wanted to take the profits to show that borrowing was actually lower.”

It was a devil's deal. When the agreement on quantitative easing was reached, Darling promised that the government would pay for any losses incurred by the Bank on the gold bonds, to prevent a black hole on the central bank's balance sheet that could distort the decision-making process.

spending the proceeds from quantitative easing during good times, it only made it more painful to make up for those losses when the economy tanked.

Lord Macpherson, who once compared QE to “heroin,” says: “It made it inevitable that you would have to pay for those losses later. Had the ring fence remained in place, losses would now be much easier to absorb.»

Profits will eventually rise to £123.8 billion at their peak in September 2022.

By that time, Osborne was long gone. His promise to spend QE proceeds only on debt repayments has also fallen by the wayside.

Andy King says: «Austerity and fiscal rules went hand in hand during the Osborne years, and then in particular you can see that the 2019 government wanted to end austerity and increased spending.»

«Over time Further, post-Osborne, fiscal targets have continued to become increasingly lenient, and the margin relative to them has continued to shrink.»

Although the gains from quantitative easing peaked just over a year ago, the rapid rise in interest rates since since then has brought with it a remarkably rapid change in the government's fortunes.

Losses from quantitative easing occur when the interest the Bank pays to commercial creditors exceeds the yield on government bonds, or when the bonds are sold at a loss.

< p>The Treasury has to make up the difference—and it has to pay it quickly. Last year alone, it transferred £29.1 billion to the Bank.

Deutsche Bank notes that “no other major central bank has had to record such losses as a direct and immediate impact on public finances.”< /p>

Andy King says: “It has been recognized that you go up a hill and then come down again. But the best way to deal with it at that time is to leave the money in the APF [asset purchase vehicle], because then no one can get it.»

Alas, this money is spent, and Jeremy Hunt is trying to find new ones funds to make up for this shortfall.

Sanjay Raja, Deutsche Bank's chief UK economist, said the bank's decision to aggressively start selling bonds back into the market also added to the bank's losses. taxpayer.

Bond prices fall as yields rise. High interest rates push yields higher and thus lower bond prices. This means the Bank is selling most of its debt at a loss.

Official figures show that this year alone the Bank has suffered losses of £11.7 billion on active gold sales alone.

Deutsche Bank says it could limit those losses by being more selective about the bonds it sells. For now, he follows a strict rule of thumb that sales are split equally between short-term, medium-term and long-term debt.

The bank is losing much more money on its long-term bonds because interest rates are «significantly higher than when they were purchased,» Deutsche Bank said. So long-term debt, traditionally favored by pension funds, is now particularly unloved.

Most of the Bank's sales losses — £7.5 billion — came from long-term debt of more than 20 years. . According to Deutsche Bank, this represents a 50% loss at the point of sale.

The bank is trimming its gold bond portfolio based on value rather than volume, targeting £100 billion a year to be allocated between maturing bonds and funds that are not reinvested and active sales.

Faced with a 50% loss on some bonds, the target suggests the Bank will have to sell twice as many gold bonds at a discounted price to reach the target.

This creates a “disproportionate loss” that Deutsche Bank estimates is costing taxpayers an extra £15 billion a year. -year due to heavy selling alone.

Raja says the losses would have been spread more evenly if the securities in question had simply been allowed to mature rather than crystallize today's sharp losses through selling. He emphasizes that the money transferred to the Bank is money that cannot be spent on other things.

“The extra cost of aggressive QT [quantitative tightening, as bond deployment is known] increases the Chancellor's debt burden, leaving him with some room for spending or tax cuts in the short term, especially given that he has a narrow margin to meet his debt rule «.

Insiders say an analysis published in December by Deutsche Bank highlighting flaws in the QT design has attracted the attention of the Treasury, with officials asking questions about how the scheme can provide better value for money.

QT decisions are made. A bank with operational independence. But Chancellor Jeremy Hunt stressed in recent conversations with Bailey that value for money remains paramount.

Lord Macpherson believes it will be «difficult to change the rules» now, «especially because the government has made profits in good times «.

» Just because it incurs losses, it cannot now change the way reserves are rewarded.

But he adds: “I imagine there will be increasing political pressure to do something about this, either by putting pressure on the Bank, which I think would be undesirable, or by potentially taxing the banks. more who have been the beneficiaries of these policies.»

Andy King, who left the OBR this summer, says: «The lesson I would take is that when it comes to political economy and all that related to public finances, having a pot of money is untenable. It will be spent.

“And it's unfortunate that the reserve compared to budgetary goals is seen as just a pot of money, and not as something that you accumulate, because the future is uncertain. Nobody looked at the profits from QE and said, well, they reached £124 billion, so the cushion must be at least £124 billion.

“There was a commitment made a long time ago, but it fell by the wayside.” plan. And the price made itself felt at a very bad time.”

Свежие комментарии