Shoppers visiting Sainsbury's supermarket in the late 90s were faced with an unusual sight. Next to the melons and dishwasher soap was a red telephone that you could use to “call the banker.” The ploy was part of Sainsbury's bid to become a full-fledged bank.

In theory, the venture made sense: Sainsbury's was a trusted brand and was regularly visited by millions of customers. But in practice, going beyond fruits and vegetables has proven difficult.

Fast forward to today, and the dream is over. Sainsbury's has halted its foray into the banking sector after announcing plans to wind down its financial services operations.

The retailer said it was planning a «phased exit» of Sainsbury's Bank following a strategic review. There will be no immediate changes to the products and services it provides to customers.

The supermarket is now considering a number of options, including transferring the business to a financial services provider, which could continue to offer banking products. under the Sainsbury's brand.

The move promises to end almost three decades of Sainsbury's direct banking and follows rival Tesco's recent move to explore the sale of Tesco Bank.

The exit of Britain's two biggest supermarkets from the banking world highlights the difficulty of competing with the big four — Barclays, Natwest, Lloyds and HSBC.

“At the end of the day, what do you want? «You wouldn't buy potatoes from HSBC, probably because you're not sure they have any special ability to sell potatoes.»

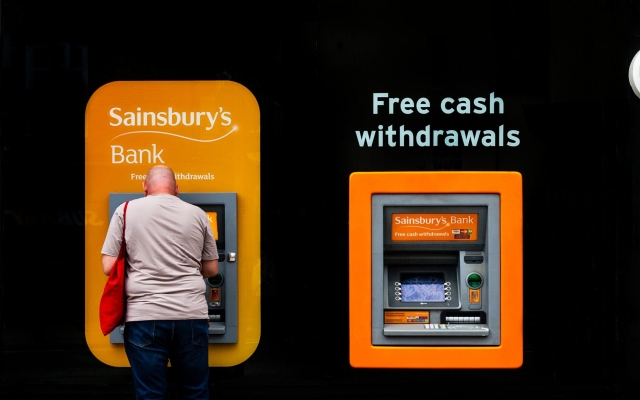

Sainsbury's entered the financial services industry in 1997 and today has approximately 1.9 million customers. His bank offers a wide range of products, including credit cards, insurance, loans and savings accounts. The bank is best known for its orange ATMs, of which there are approximately 1,350 across the country.

“I remember when Sainsbury's was created and it did well but it never succeeded,” says Sir Philip. “It was a customer service challenge to have ATMs in supermarkets so people could transact with cash. But it is clear that this business has never reached scale and probably never will.”

Sainsbury's ATM network has become smaller valuable amid the shift to digital banking and an increasingly cashless society. Photo: GRANT ROONEY PREMIUM/Alamy Stock Photo

Sainsbury's ATM network has become smaller valuable amid the shift to digital banking and an increasingly cashless society. Photo: GRANT ROONEY PREMIUM/Alamy Stock Photo

Questions about Sainsbury's commitment to its financial services division have been debated for many years.

The supermarket previously tried to sell Sainsbury's Bank, attracting interest from potential buyers such as Centerbridge Partners, but negotiations ended in 2021 after it concluded the sale did not benefit shareholders.

< p>Tesco is similarly trying to sell off pressure on its bank, which employs 3,540 people and has 5.2 million customers. The company recently hired Goldman Sachs to explore a sale, and HSBC, Lloyds and Barclays have been flagged as possible suitors.

Why did supermarkets open banks in the first place? In the late 1990s the financial services sector was «very profitable», says Sir Philip. “Many people have entered financial services in general and banking in particular, either as new entrants or to strengthen an existing brand.”

Banking has also offered new growth opportunities for supermarkets over a period. frantic expansion.

As former Tesco boss Sir Terry Leahy previously said of his supermarket's banking plans: «It's as if the shark can't stand still and will drown. We need to keep going.”

However, when the financial crisis hit, “the change in perception of the attractiveness of the industry was absolutely fundamental,” says Sir Philip.

Supermarkets initially hoped it would be possible to lure customers away from incumbents, given the damage done to the reputations of many of the big banks. Ultimately, such a shift did not take place.

“Despite best efforts to penetrate the market, the traditional Big Four clearing banks still have a very high share of all current accounts,” says Sir Philip.

However, this has not stopped many from trying to break into the market over the years. The strange cocktail of selling baked beans and mortgages is a unique mixture in the UK, but it has a long history.

The Co-op Bank, which is currently in talks to merge with Coventry Building Society, offered financial services as part of the Co-op supermarket chain for 140 years before it nearly collapsed in 2013.

The hedge fund bailout led to the bank being spun off, although it managed to retain the Co-op brand.

M&S also took the risk of providing financial services with M&S Bank, although the lender is ultimately controlled by HSBC.

This gives it an advantage over standalone lenders such as Sainsbury's Bank, which was originally founded with support from Bank of Scotland before the supermarket took full ownership in 2014.

For upstart challenger banks It has always been difficult to compete with larger lenders. Products such as mortgages, loans and current accounts are commodities, meaning price is a critical factor in attracting customers.

Large banks, with their scale, can often guarantee better prices than smaller players .

«There's no good in being good, you need to be better if you're challenged,» says Shore Capital banking analyst Gary Greenwood. .

Barclays, Lloyds, Natwest and Lloyds dominate the multi-trillion-dollar banking world, leaving Tesco Bank and Sainsbury's Bank part of the total market.

«They weren't the focus in a material sense,» says Jefferies analyst Joseph Dickerson. «They weren't trying to differentiate themselves on the liability side of their balance sheet, such as with checking accounts or some unique savings offerings.

«They didn't approach the scale of any of the big banks.'

The move from bank branches to digital banking has also eroded the advantage supermarkets had in having a significant network of stores.

When Tesco and Sainsbury's opened their banks in 1997, there were no smartphones. The cost of setting up a branch in a supermarket was relatively minimal.

Now that competitive advantage is gone.

“Life has changed,” says KBW banking analyst Ed Firth. “Banking used to be a branch business, and so supermarkets had a competitive advantage because they actually had branches everywhere.

“But it's no longer a branch business. You don't have the synergy that you had when they started.»

Like Sainsbury's original red telephones, the idea of supermarket financial services is looking more anachronistic every day.

Свежие комментарии